Quebec more stringent with tax exemptions

At the end of June, Heidi Diabo was trying to purchase a door at the CANAC hardware store in Beauharnois, when she was left rattled by an interaction with an employee she felt was the result of her being visibly Indigenous.

That was when the clerk told her that she would have to pay Quebec Sales Taxes (QST) in Beauharnois, as it was outside the area where there is the tax exemption.

“I was quite alarmed to hear that we’re out of the jurisdiction. So I looked at him, I said, ‘since when is this becoming a jurisdiction thing?’” said Diabo.

“I said ‘I’m Native. We used to own everything.’”

Diabo said she was more upset about feeling like the employee had brought up taxes because she was Indigenous than having to actually pay the QST.

“I don’t mind paying the tax if I have to, but that’s not what the point is. I’m trying to exercise our rights,” said Diabo.

She added that this had not been the first time this happened to her in a business off-reserve.

“I’ve had this happen to me multiple times. They’ll ask me straight out, ‘what’s your band number?’” said Diabo.

“You normally wouldn’t say that to any other person, to say something like ‘you want to buy something, are you French?’”

Eric Langevin, director of the CANAC store in Beauharnois, said that this had been an unfortunate misunderstanding, and he was sorry that Diabo had felt that she had been disrespected.

He said that according to the clerk, the intention had actually been to inform Diabo that she would have to pay taxes because of Revenu Quebec’s rules, not to assume that she was Indigenous by doing so - Langevin added that the clerk knew she was from Kahnawake due to her CANAC account information.

“I assure you the employee’s intention was not to disrespect the client, quite the contrary,” said Langevin.

“The goal was to inform, not to profile.”

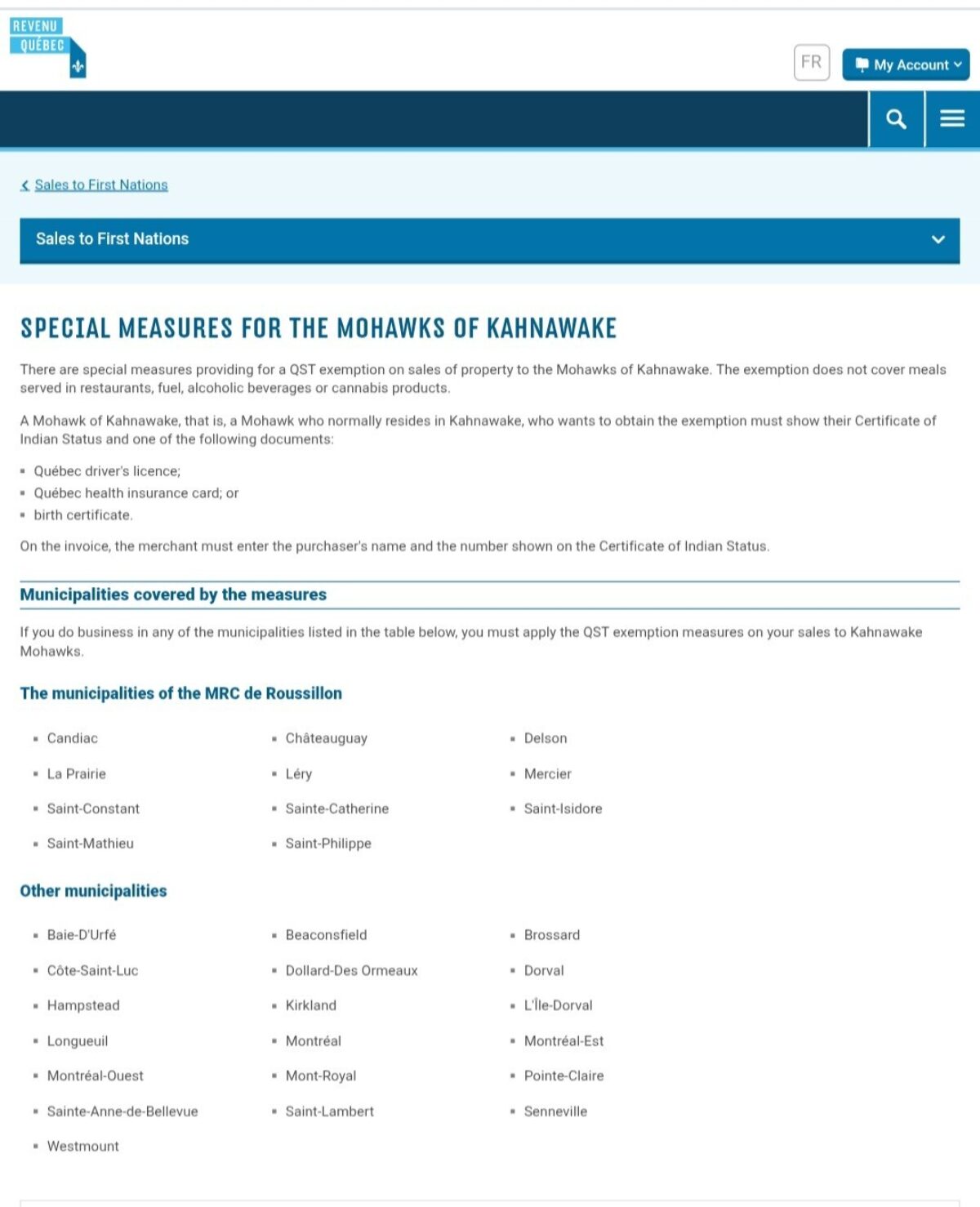

This is all a result of Revenu Quebec’s stringent tax exemption rules, the “Special Measures for the Mohawks of Kahnawake,” which legislates where exactly people from the community are eligible to not pay the QST.

Beauharnois is not in the regional municipal county (MRC) of Roussillon, and it is not covered by the “other municipalities” that include Montreal and Longueuil, for example.

That’s despite Beauharnois being about the same distance by car as Longueuil, and many shoppers from Kahnawake choosing to go to stores in Beauharnois.

Langevin said that because of the rule, he has attempted to direct people from the community to CANAC stores in La Prairie or St. Hubert, which are a part of the area covered by the Special Measures. He added that the Special Measures also include a provision where delivery to a home address in Kahnawake would exempt buyers from the QST.

He also said that he had spoken with a contact within the Mohawk Council of Kahnawake (MCK) a few years ago to try to inform the community of having to pay taxes in Beauharnois because of other incidents at the store.

Sign up for email updates from The Eastern Door

In the past, many businesses outside the Special Measures zone actually did give the QST exemption, said Tricia Collier, Tax and Estate Planning advisor of the MCK’s Client-Based Services.

“That has been changing. Revenu Quebec is now rigorously enforcing the agreement. This means that when a retailer submits their tax remittance to Revenu Quebec, the documents are being processed according to the rules of the agreement. Any remittance that does not meet the agreement in place will be denied, leading to the retailer paying the exempted amount out of pocket,” said Collier.

“As more retailers are made aware of the specifics of the agreement, they are following it precisely. The result is that retailers outside of the agreement zone are no longer accepting point-of-sale tax exemptions for Kahnawa’kehró:non.”

Collier said community members are encouraged to get in touch with her for more information or if businesses that are in the areas covered by the Special Measures do not give the QST exemption. They can do so by writing to [email protected] or by calling 450-638-0500, ext. 59342.